A Closer Look at Historical Bear Markets & The Cure

Monday, September 26th, 2022

My goodness; stocks are taking a terrible beating these days. From the way the market is behaving, one might think that some of the world’s largest and most profitable companies are suddenly becoming dramatically less valuable. Are they all laying off workers, slashing prices, closing factories and declaring imminent bankruptcy?

If this is sending you to anxiously scanning the headlines, don’t bother; none of that is happening. Stock prices have never been a precise indicator of what companies are worth. They are a very good indicator of what people are willing to pay for their shares, and right now there seems to be more sellers than buyers.

Why? The reasons for bear markets are seldom rational—which, of course, is why bear markets end and stocks return to (and always, in the past, have surpassed) their original highs. What’s happening right now is not unlike what happens when one of our children is diagnosed with an illness, and the remedy is a daily dose of some awful-tasting medicine. The illness, in this case, is inflation, which absolutely has to be cured if we are to experience a healthy economic life. Few things are worse than having the money you’ve saved up deteriorate in value at double-digit rates, which is precisely what has been happening this year.

The cure, which any child will tell you is more unpleasant than the illness itself, is the U.S. Federal Reserve raising interest rates, which is its way of reducing the amount of cash sloshing around in the economy. Rising consumer prices, just like rising stock prices, come about when there are more buyers than sellers. Reducing the available cash reduces the number of buyers in relation to sellers (ironically, both in the consumer marketplace and on Wall Street), and finally slows down the inflation rate to manageable levels.

We can already see how this works in the housing market, where, just a few short months ago, multiple would-be buyers were bidding against each other to pay more than the asking prices. As mortgage rates have risen, the frenzy has completely dissipated. The process takes longer in the consumer marketplace at large, but you can bet it’s working behind the scenes.

Doesn’t less spending mean less economic activity? Doesn’t that lead to a recession? The answers, of course, are yes and maybe. But at this point, a recession might not be all bad for the economy. Recessions act like a cleansing mechanism, exposing/eliminating waste and inefficiency, ultimately creating a healthier economy when we come out the other end.

So right now we’re taking our medicine, and boy does it taste awful. We are also, collectively, suffering an economic illness. Anybody who has come down with a bug and taken medicine to cure it knows that the former unpleasantness doesn’t last forever, and therefore neither does the latter.

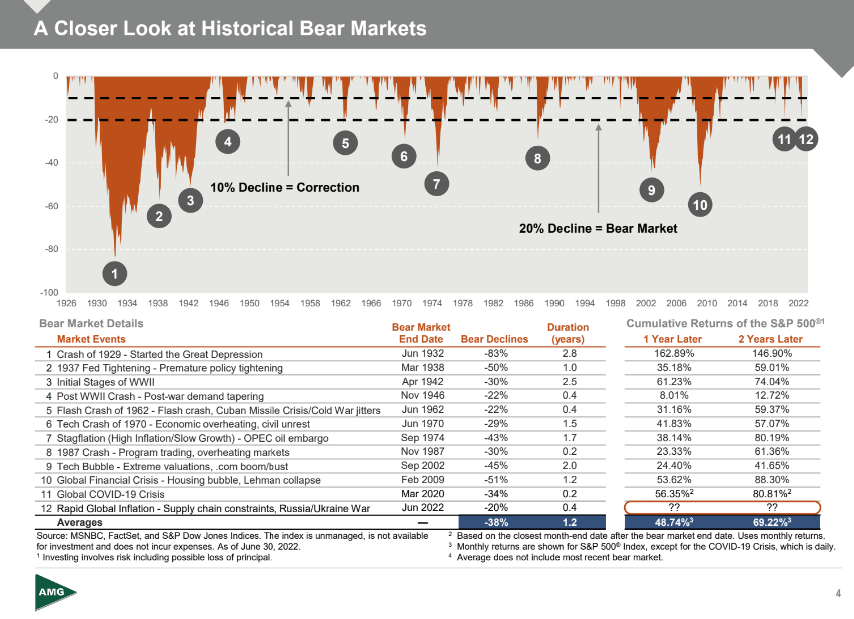

The chart above lists every bear market since 1929, the magnitude of decline, duration of the bear market, and cumulative return of the S&P 500 1 and 2 years after.

While volatility is normal, the longevity and sharpness of each bear market varies. As we look to returns 1-2 years after a bear market, we can agree with Warren Buffet, "Look at market fluctuations as your friend rather than your enemy; profit from the folly rather than participate in it."

We appreciate your continued trust in our team and we welcome you to reach out should you have any concerns.

With gratitude,

Your Team at Beacon Financial Planning

SOURCES:

https://www.nytimes.com/2022/

AMG Funds: A Closer Look at Historical Bear Markets

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE PERFORMANCE. All investing involves risk and costs. Your advisor can provide you with more information about the risks and costs associated with specific programs. No investment strategy (including asset allocation and diversification strategies) can ensure peace of mind, guarantee profit, or protect against loss. Please contact us if you have any changes that may impact your financial situation. The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security.